Download der Management Summary

Management Summary of the Data Center Impact Report Germany 2024 [DE]Data Center Impact Report Germany 2024

The comprehensive study, which was initiated by the German Datacenter Association, sheds light on the status quo and the decisive influence of German data centers on digital transformation, economic development and sustainability efforts within Germany and beyond.

The results of the study paint a positive picture of the data center sector in Germany. Despite challenges such as the limited availability of electricity and space, regulatory hurdles, bureaucracy and a shortage of skilled labour, the market is experiencing significant growth. This development is being driven by the increasing demand for cloud services, big data analytics and the integration of AI technologies.

Download the full Data Center Impact Report Germany 2024 here.

The most important findings of the study are summarised in the management summary and classified from the perspective of the German Datacenter Association.

Data Center Impact Report Germany 2024

The Data Center Impact Report Germany 2024 looks at the dynamic growth and economic impact of the German data center industry in 2024 and beyond. It highlights the industry's central role in supporting digital transformation in various sectors and emphasises its contribution to strengthening Germany's digital infrastructure. The analysis shows the accelerated expansion of the sector, driven by the increasing demand for cloud services, big data analytics and the integration of AI technologies.

However, no precise figures were previously available on the number of data centers in Germany and the IT capacity they provide. Similarly, employment figures, data on investments and the industry's contribution to gross domestic product were based on estimates. In order to create a solid database and identify relevant developments, the German Datacenter Association (GDA) has commissioned a study, the results of which are now available to you. After all, potential can only be realistically assessed if reliable data is available for decision-making.

The study commissioned by GDA presents quantitative results based on various research methods. A secondary survey was used to establish a solid database for colocation and hyperscale data centers in order to identify and understand relevant trends and developments. In addition, two surveys were conducted: One with 29 leading decision makers in colocation data centers and another with 203 decision makers in enterprise data centers.

From now on, the data will be updated on an annual basis to document the current status of the market. In addition to the existing data, we will analyse further key figures in the coming years.

We hope you enjoy reading the Data Center Impact Report Germany 2024 and look forward to sharing our findings with you!

Data centers build the future: investments in reliable and secure infrastructures

Data center industry is booming: continued growth despite challenges

The key to success: political foresight for sustainable development

Seit 2010 hat sich die benötigte Rechenleistung aufgrund der fortschreitenden Digitalisierung aller Lebens-, Wirtschafts- und Forschungsbereiche verzehnfacht, was die zentrale Rolle von Rechenzentren für die hochverfügbare Bereitstellung digitaler Dienste und die Wahrung der digitalen Souveränität Deutschlands unterstreicht. Vor dem Hintergrund des deutschen Energieeffizienzgesetzes und der damit verbundenen Effizienzanforderungen, wird die Notwendigkeit deutlich, durch Initiativen wie die Studie der GDA eine solide Datenbasis zu schaffen, um den Markt transparent zu machen und Potenziale realistisch einschätzen zu können.

Anna Klaft |Vorstandsvorsitzende der German Datacenter Association

Data centers build the future

Investments in reliable and secure infrastructures

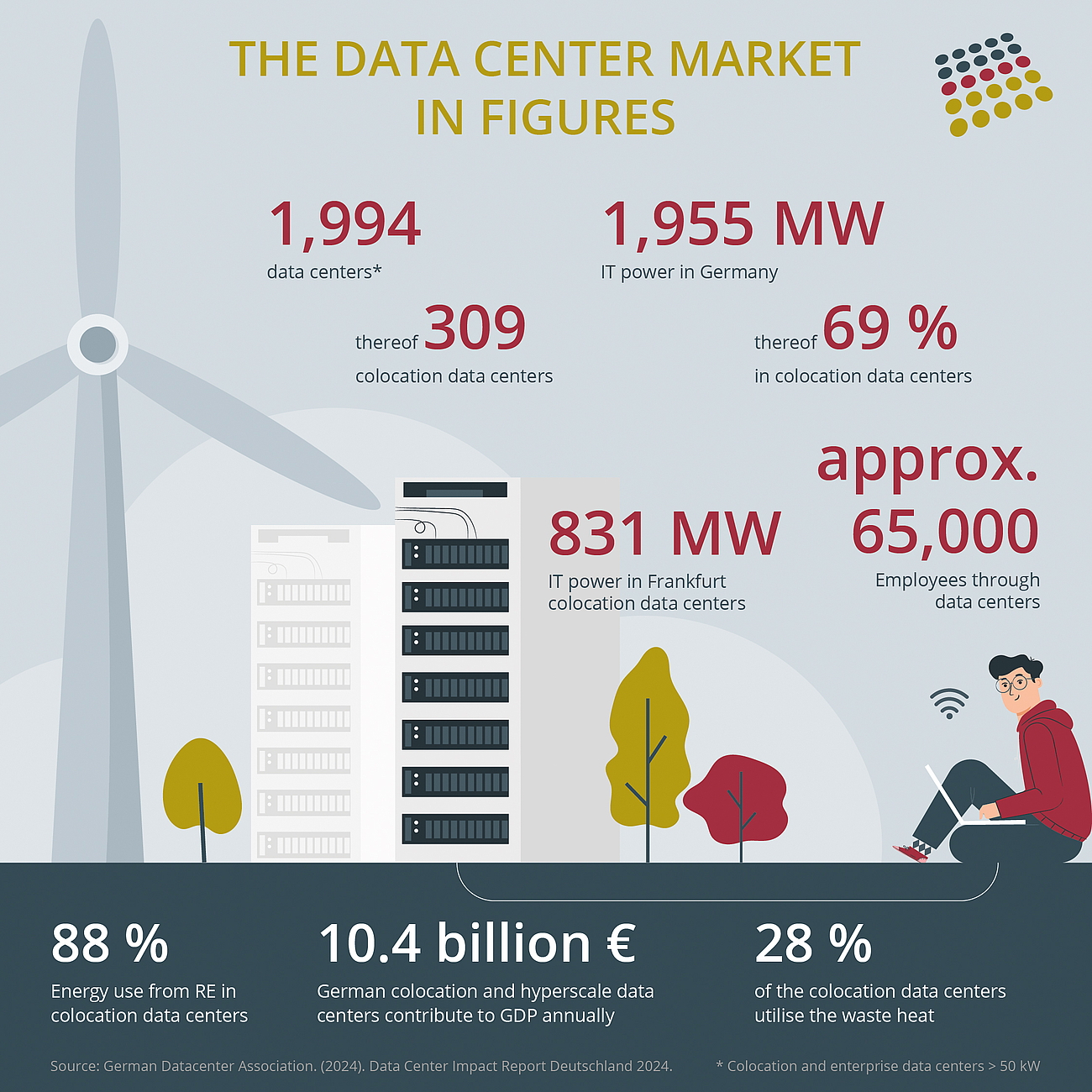

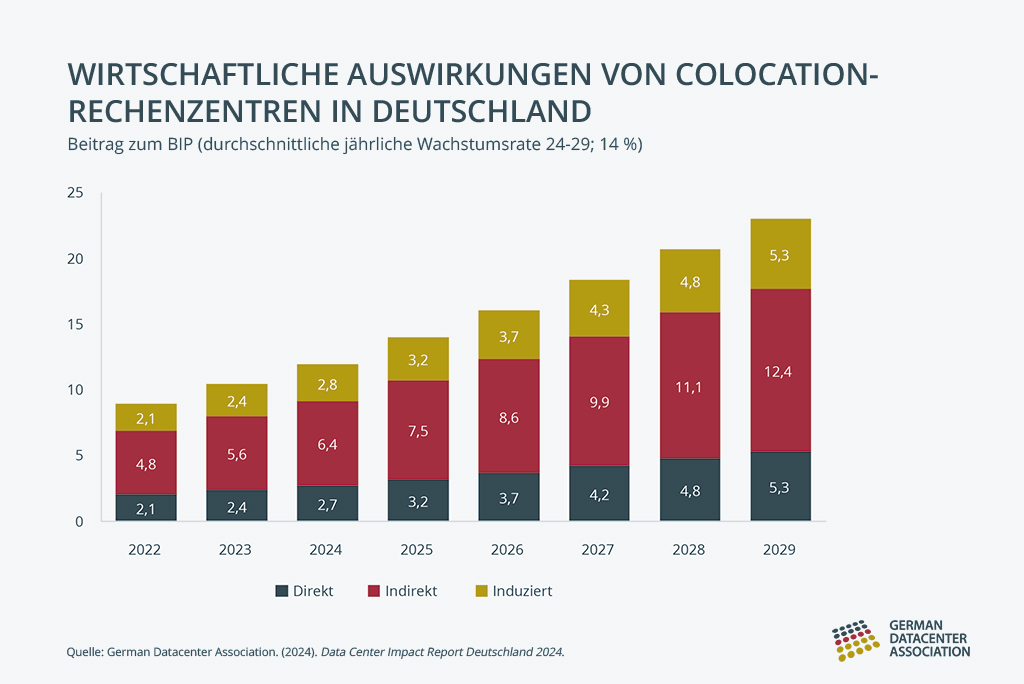

The data center sector is experiencing dynamic growth and makes an important contribution to the German economy. It forms the basis for efficient digital development in the country: It is predicted that the economic contribution of this sector to the gross domestic product will grow to 23 billion euros by 2029. In addition, it promotes the creation of around 65,000 jobs in this sector and makes considerable investments that benefit the local economy.

Based on a conservative growth model, this study forecasts continuous investment of around two billion euros per year in the expansion of colocation and hyperscale data centers. If, on the other hand, the predicted growth in IT capacities is quantified using market values for construction costs for the expanded data center, estimated average land prices and average space efficiency, investments of over 24 billion euros can be expected for the expansion of colocation capacities by 2029. Added to this are the 4.2 billion investment programmes of hyperscalers Google and Microsoft, which will last until 2030. Plus the costly server infrastructure.

Data centers promote energy transition

Industry actively involved in the expansion of renewable energies in Germany

The industry is leading the way in the use of electricity from renewable energy sources. Already today, 88% of the electricity consumed by colocation data centers comes from renewable sources, underlining the sector's efforts towards sustainability in the technology industry.

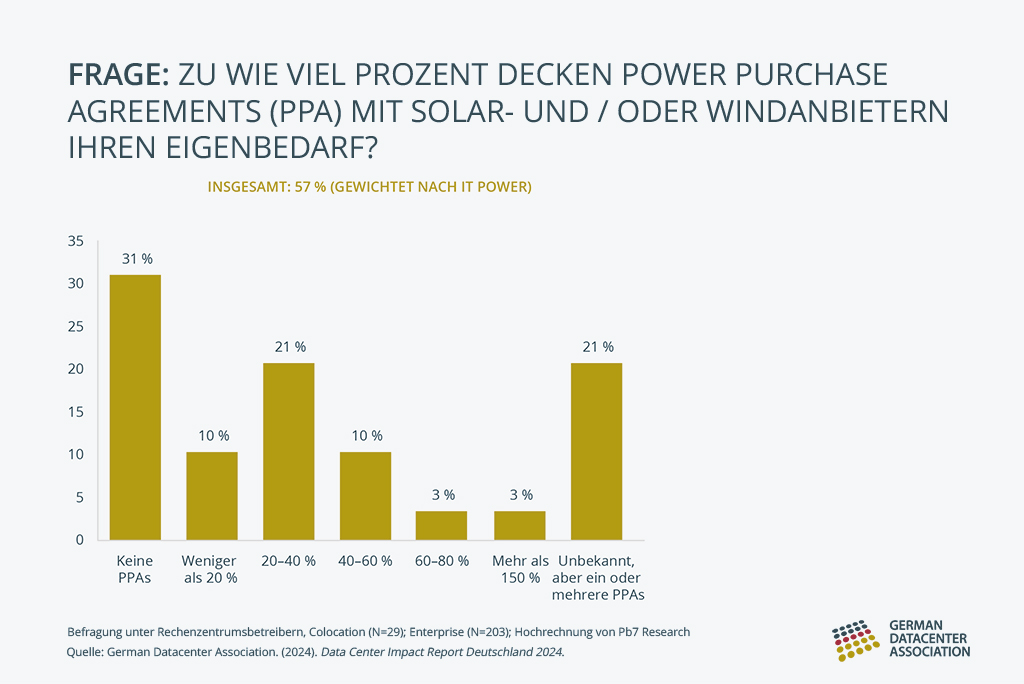

69% of the colocation companies surveyed stated that they purchase electricity via one or more Power Purchase Agreements (PPA). Through this power purchase agreement, the customer commits to purchasing electricity directly from a renewable energy project over a longer period of time. In return, they receive a reduced electricity price. Through PPAs, the data center industry is strongly committed to the expansion of renewable energies in Germany - many of these investments would not be possible without the financial security provided by PPAs.

Through the intelligent use of waste heat, data centers can contribute to a significant reduction in CO₂ emissions and at the same time increase the efficiency of energy use. This is an essential step towards achieving the goals of the Paris Agreement and realising the vision of a climate-neutral future.

Illustrations designed by Freepik.

Data center industry is booming

Continued growth despite challenges

This growth is being driven by the increasing demand for digital services, cloud computing and the digital transformation in all sectors. The Internet of Things (IoT), the 5G transmission standard and developments in the field of artificial intelligence are ensuring that the demand for data processing is increasing exponentially. It can be assumed that the IT capacity of colocation data centers in Germany will increase from the current 1.3 GW to 3.3 GW by 2029.

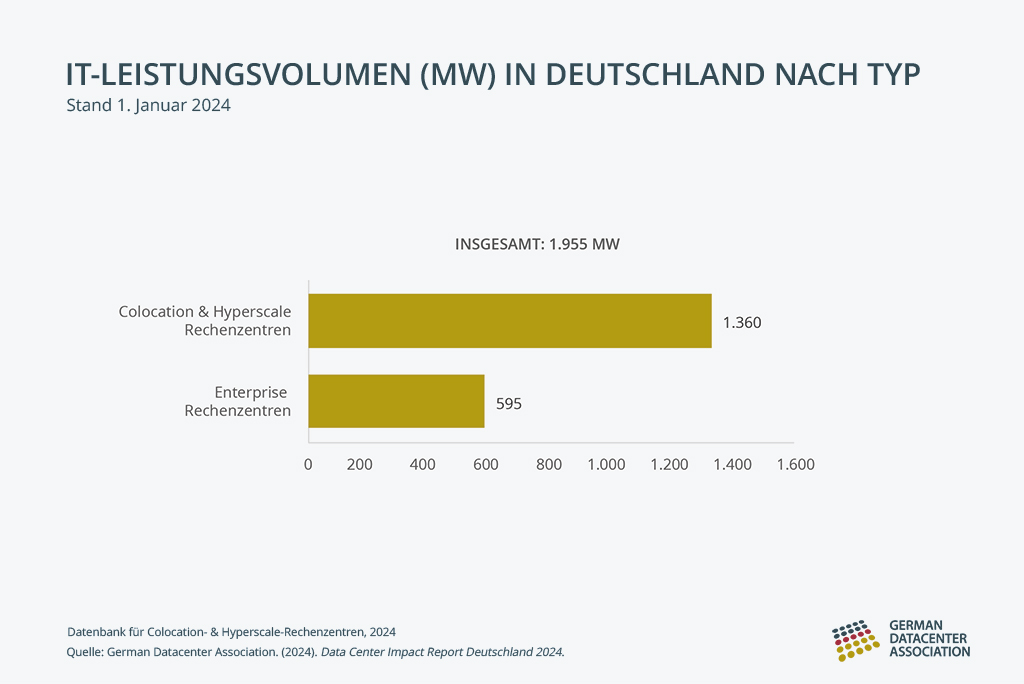

In this context, data centers in Germany are constantly working to optimise their energy efficiency and sustainability and to reduce their environmental impact. The majority of IT power in Germany, around 70% (1,360 MW of a total of 1,955 MW), is provided by colocation data centers, which have energy efficiency advantages over enterprise data centers due to their economies of scale.

Data centers are the key to success

Political foresight for sustainable development

The sector faces a variety of challenges, such as the scarce availability of space and electricity, high electricity prices, complex authorisation procedures and complex regulations. Despite all the challenges, Germany has significant locational advantages that are decisive for the establishment of data centers and promote the growth of the sector.

Together, these complex challenges can be overcome and the potential of digital infrastructures can be fully utilised. Political initiative and an in-depth understanding of the specific requirements of the sector are essential to ensure the basis for further growth and to secure investment in the German infrastructure. The publication of the "Data Center Impact Report Germany 2024" provides a sound basis for dialogue with political and economic decision-makers in order to strengthen the framework conditions for data centers and thus Germany's position as a location for business and innovation.

The international location advantage that already exists must not be jeopardised. For this reason, the GDA continues to advocate close dialogue with politicians and administrators at local, national and European level in order to improve the framework conditions in the interests of the industry.